Think about this: Do public wireless carriers need to own their own networks?

Mobile network operators (MNOs) today face daunting technical and financial challenges to continuously upgrade and expand their radio access network (RAN) and core switching infrastructure, especially with 5G in the offing. Deploying macrocells and small cells in various frequency bands to serve myriad new use cases requires a lot of infrastructure (see, More Frequencies, More Uses, Better UX!).

Yet carriers are in a cash flow crunch, struggling to fund this expansion in the face of flagging revenue growth and unprecedented debt levels while trying to keep shareholders happy. (see, Can Carriers Afford 5G?)

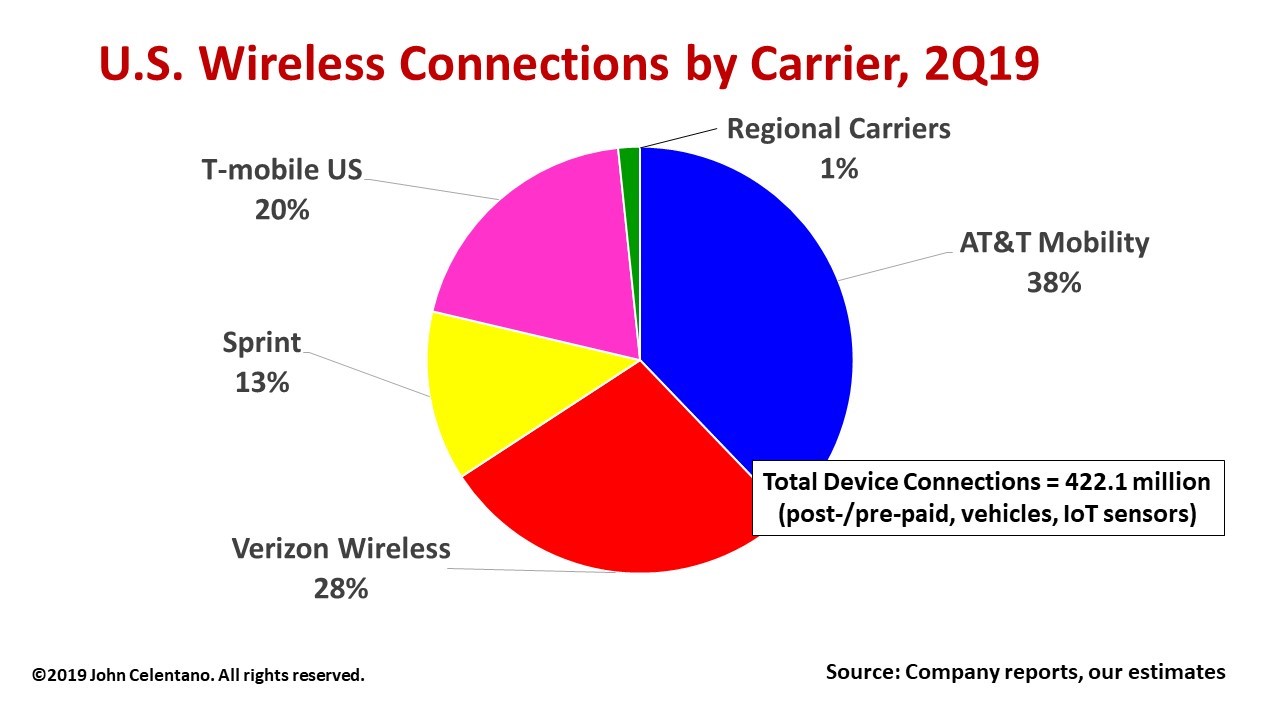

Does network ownership really matter? At one time, it did. A giant, vertically-integrated, regulated monopoly, the AT&T Bell System designed, built and operated a ubiquitous local/long distance network intended to do one thing – deliver circuit-switched voice service to any phone on the planet. “The System is the Solution” was the tagline. Eventually, anti-trust action forced the monopoly break-up with AT&T divesting the local service Baby Bells while keeping Long Lines, Network Systems and Bell Labs. Since then, AT&T and Verizon have reconstituted large parts of the old Bell System to the point where they together control two-thirds of all U.S. wireless connections. They still think their competitive advantage comes from proprietary NextG networks. Their ads suggest: ‘My network is bigger and badder than yours!’ Yet building and operating such networks requires massive capex infusions to meet exploding mobile data demand even with no revenue growth. That model is no longer sustainable.

Prevailing market and economic forces, not antitrust issues, now are driving considerations for another Bell breakup. One solution would be to separate the carriers’ infrastructure business from their services business.

Here, all MNOs would spin off to a neutral company, say, InfraCo, their existing infrastructure (RAN/CORE) assets (and probably debt) along with engineering and operations people, and license use of current spectrum holdings. InfraCo invests the capital to build and operate an advanced network platform everywhere it is needed. Carrier ownership in InfraCo would be proportional to their respective contribution. InfraCo could be a private company or publicly-held to raise its own capital and/or receive contributions from its owners. InfraCo could also be regulated.

All MNOs become Mobile Virtual Network Operators (MVNOs), say, ServiceCos, that buy at wholesale rates coverage and capacity from InfraCo wherever and whenever they need it. Each ServiceCo resells multimedia services at retail rates to customers in various markets: urban/rural, outdoor/indoor, Enterprise/residential. This sets up a more competitive environment with creative service packages and pricing that customers want. Other MVNOs and neutral hosts could also buy from InfraCo.

Will it work? Certainly, there are pointers. Carriers sell their towers to raise cash then lease back RAD center space from tower companies. (see, AT&T CEO Says Selling Towers Will Help Pay Down Debt) MVNOs already lease network capacity from the MNOs then resell wireless services under their own brand. Citizens Broadband Radio Services (CBRS) is a shared spectrum concept that promises widespread indoor and outdoor use. Sprint subcontracts Ericsson to build and run Sprint’s 4G LTE network. Most telling, tower companies already manage more carrier infrastructure – towers, small cells, fiber, DAS. Can RAN and CORE be far away? (see, The Rise of Wireless Infrastructure Companies).

Bottom line: MNOs have hit the wall in their ability to fund network modernization in the face of escalating mobile data demand. A new operational paradigm is imperative.

John Celentano is Inside Towers’ Contributing Analyst. He can be reached at: [email protected]

John Celentano is Inside Towers’ Contributing Analyst. He can be reached at: [email protected]

By John Celentano for Inside Towers

September 27, 2019

Reader Interactions